By Nicole Downer Managing Partner MV Credit Partners LLC

By Nicole Downer Managing Partner MV Credit Partners LLC

Navigating Choppy Waters

After working through an incredibly eventful year in the global economy, investors in private credit benefitted from the stable and consistent yields expected of the asset class. That was welcomed by investors, who went through a rollercoaster in the public markets.

Private credit has grown from being specialist and niche asset class to a more established component of a diversified investment portfolio, from a sub $100bn asset class in 2000, to a greater than $800bn in 2020. This growth is not expected to slow given the continued hunt for yield.

Drawing on over 20 years of experience, we will discuss how managers can take advantage of opportunities and mitigate risks during the downturn. We will explore which strategies are most likely to provide attractive risk-adjusted returns and why now is a particularly attractive time to invest in private credit.

Finally, we will discuss how an ESG conscious investor can utilise private credit to create a more sustainable approach to investing

Why Private Credit?

Given the “lower for longer” interest rate environment, private credit funds have drawn significant inflows since the Great Financial Crisis (“GFC”). Prior to the GFC, investment banks were the typical mid-market lenders of choice and this dynamic has since progressed. Given the increased regulation and introduction of Basel III this led to a retrenchment of the banks from the market. This has coincided with investors seeking higher yields and diversification from non-traditional asset classes such as private credit.

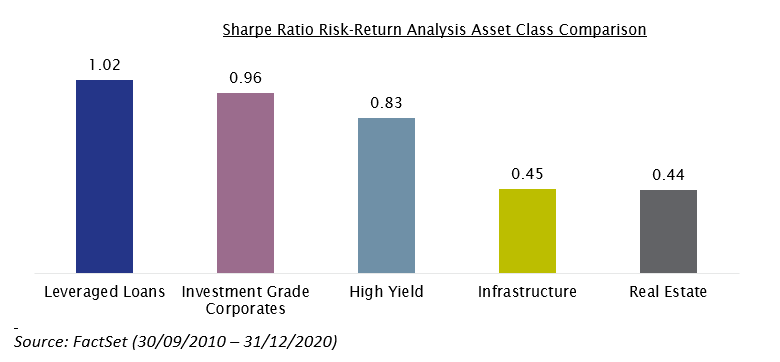

In comparison to high yield (an asset class often look at alongside senior loans), leveraged loans have consistently delivered higher risk adjusted returns, owing to their low volatility and stable return streams. The below chart demonstrates the strength of the asset class in comparison to other credit classes.

In addition to the above, high yield bonds typically have higher default rates and lower recovery rates than leveraged loans. For example, between 1983 – 2019, leveraged loans had a recovery rate of 66% vs. 55% for high yield bonds. When a default does happen, loan holders typically receive more of their money back than bond holders.

The Pitfalls of Distressed Credit During the Downturn

As investors seek attractive opportunities to time this moment in the cycle, they may look to opportunistic strategies such as distressed credit. However, we believe that distressed lending has its limitations.

Setting aside the significant ESG concerns with distressed credit managers’ investment strategy (which can be viewed as more confrontational towards stakeholders than collaborative with them, and as potentially adding challenges to borrower companies in a period of stress), there may be factors negatively impacting their performance. Following the last downturn, private equity sponsors restricted transfers to distressed private credit funds, which may limit the opportunities available to distressed funds, even in a downturn.

Additionally, distressed buyers may invest in more cyclical industries such as hospitality, retail and automotive, as the current downturn has negatively impacted these industries. However, we believe that this downturn and the covid-19 crisis may dramatically change the business models of such industries, potentially over the long term. This makes distress lenders’ investments not comparable on a like-for-like and risk adjusted basis with traditional private credit lending strategies

Why Now?

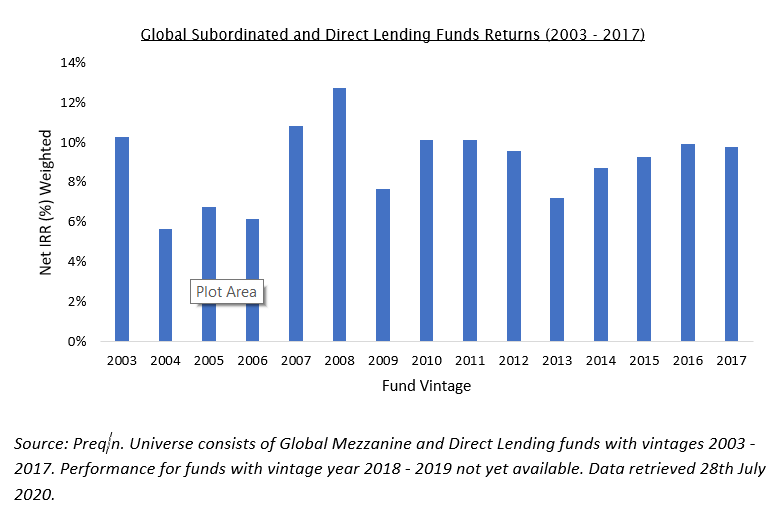

Following a downturn, the credit cycle enters a period of repair and recovery. After the GFC, demand amongst private credit managers for new credits rose slowly and MV Credit expects a similar trend following the current downturn.

This period was marked by better economics which drove attractive returns for private credit, with 2008 vintages notable for their high returns. Whilst this data is for global private credit funds, we expect European funds to follow a similar trend. We believe that 2020/2021 vintages will also be high returning in a similarly favourable environment.

Despite a downturn presenting challenges for private credit managers, new investments are expected to generate higher yields, with more favourable lending terms and in credits that will be reviewed against a “post-Covid” economic environment. Coming out of the downturn, we expect the strongest credits to come to market first with portfolios that invest in cyclical industries struggling and assets in more cyclical industries likely to have trouble sourcing financing.

Despite a downturn presenting challenges for private credit managers, new investments are expected to generate higher yields, with more favourable lending terms and in credits that will be reviewed against a “post-Covid” economic environment. Coming out of the downturn, we expect the strongest credits to come to market first with portfolios that invest in cyclical industries struggling and assets in more cyclical industries likely to have trouble sourcing financing.

ESG

Given the state of the market, it is expected that private credit firms, such as MV Credit, will be able to work with their private equity sponsors to create a more sustainable approach to investing. The private market is in a unique position to bring about change and continue to push for ESG.

During 2020, MV Credit invested in an ESG linked loan for a company called Kersia. Headquartered in France, Kersia is the #3 global player specialised in the formulation, production and sale of biosecurity solutions for the food industry. Kersia’s senior secured credit facility includes a bonus/malus mechanism on the applicable margin tied to the achievement of ESG KPI’s. These ESG KPI’s include the share of green products sold by the company, the recycling of packaging and the share of employees that are given the opportunity to become shareholders of the group. It also includes the requirement of providing a sustainability KPI certificate which will be certified by a sustainability auditor. We expect to see more of these types of financing in 2021 and beyond.

Conclusion

Whilst the economic outlook remains unknown, we believe the experience of the MV Credit team investing through multiple cycles (20+ years) will help to navigate the choppy waters ahead.

Article highlights:

After working through an incredibly eventful year in the global economy, investors in private credit benefited from the stable and consistent yields expected of the asset class. That was welcomed by investors, who went through a rollercoaster in the public markets.

After working through an incredibly eventful year in the global economy, investors in private credit benefited from the stable and consistent yields expected of the asset class. That was welcomed by investors, who went through a rollercoaster in the public markets.- Private credit has grown from being specialist and niche asset class to a more established component of a diversified investment portfolio, from a sub $100bn asset class in 2000, to a greater than $800bn in 2020. This growth is not expected to slow given the continued hunt for yield.

- Drawing on over 20 years of experience, we will discuss how managers can take advantage of opportunities and mitigate risks during the downturn and economic uncertainty. We will explore which strategies are most likely to provide attractive risk-adjusted returns and why now is a particularly attractive time to invest in private credit.

- Finally, we will discuss how an ESG conscious investor can utilise private credit to create a more sustainable approach to investing

About MV Credit

![]() MV Credit Partners LLP is an independently managed pan-European private credit specialist founded in 2000 with offices in Luxembourg and London. A wealth management company authorised and regulated by the FCA.

MV Credit Partners LLP is an independently managed pan-European private credit specialist founded in 2000 with offices in Luxembourg and London. A wealth management company authorised and regulated by the FCA.